Good morning. Happy Tuesday.

The Asian/Pacific markets closed with a lean to the downside. Hong Kong and China did well, but Australia, India, New Zealand and Taiwan lost ground. Europe is currently mixed, and movement is minimal. The Czech Republic and Denmark are down more than 1%; Greece and Sweden are also weak. The UK, Russia, the Netherlands and Turkey are doing okay. Futures in the States point towards a positive open for the cash market.

—————

Join our email list – get technical research reports sent directly to you.

—————

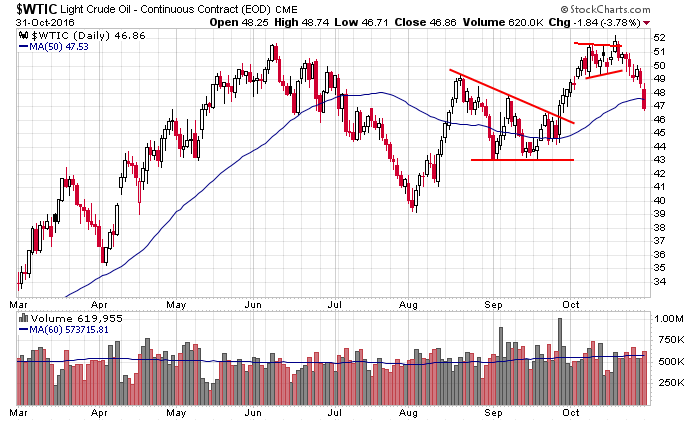

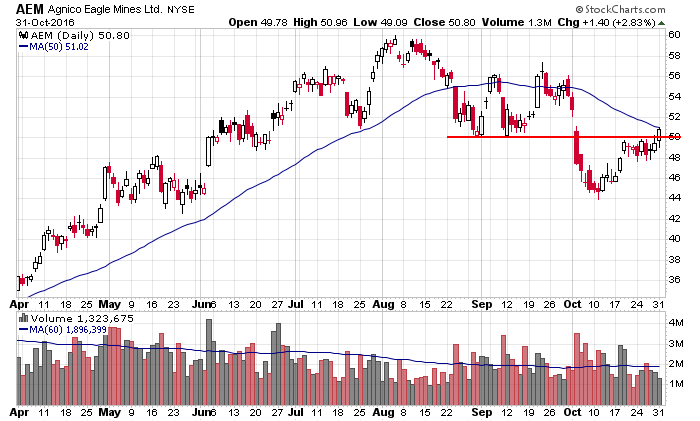

The dollar is down. Oil is down; copper is up. Gold and and silver are up big. Bonds are down.

There’s been so much chatter about the election, no one is talking about the FOMC meeting tomorrow. Yes, the Fed meets tomorrow to decide if rates should be moved up, but the lack of chatter is an indication that Wall St. believes there’s very little chance rates change – not one week ahead of the election. Tomorrow should be a nonevent – just a box that needs to be checked as earnings continue to roll out and eyes focus on next week’s election.

Beneath the surface of the indexes, which remain range bound, are oil and gold/silver are moving.

Oil got hit hard yesterday and is down premarket today. It broke out two weeks ago but couldn’t hold the gains for a single day. It bled down until yesterday when the floor got pulled out. A 3.8% single-day drop is its biggest in several weeks, and this is the first close below the 50-day MA since mid-September.

Gold and silver did pretty well yesterday and are up a bunch is premarket trading today. I’ve talked about them on the Message Board recently as groups that were in intermediate term downtrends (they’re still trading below their declining 50-day moving averages) but in the near term had decent prospects of moving up. I’m not 100% on board with a bottom being in place, but in the near term things are improved. AEM is one I’ve posted.

No big bets right now. More after the open.

Stock headlines from barchart.com…

Wynn Resorts Ltd. (WYNN +0.39%) climbed 2% in pre-market trading after it reported Macau’s gaming revenue rose +8.8% to $2.73 billion, the third straight monthly increase.

Luminex (LMNX +1.51%) rose 3% in after-hours trading after it reported Q3 adjusted EPS of 21 cents, above consensus of 20 cents, and then raised its 2016 revenue estimate to $267 million-$270 million from a July 28 estimate of $261 million-$269 million.

Twilio (TWLO -3.67%) rose nearly 2% in after-hours trading after it was rated a new ‘Outperform’ at Oppenheimer with an 18-month target price of $50.

Brocade Communications (BRCD +21.98%) was upgraded to ‘Outperform’ from ‘Sector Perform’ at RBC Capital Markets with a 12-month target price of $14.

Amkor Technology (AMKR +0.87%) climbed over 5% in after-hours trading after it reported Q3 EPS of 25 cents, higher than consensus of 21 cents, and said it sees full-year EPS of 55 cents, above consensus of 42 cents.

Lockheed Martin (LMT -0.65%) received a $536.4 million modification to an existing U.S. Air Force contract.

Tenet Healthcare (THC -2.67%) dropped over 3% in pre-market trading after it reported Q3 adjusted EPS continuing operations of 16 cents, weaker than consensus of 19 cents.

Raytheon (RTN -0.42%) was awarded a $174.7 million U.S. Defense Advanced Research Projects Agency contract that will run through Oct, 2017.

Tesoro (TSO +1.74%) lost 2% in after-hours trading after it cut its 2016 capex view to $900 million, below an earlier view of $1 billion.

Green Plains Partners LP (GPP -0.93%) reported Q3 adjusted EPS of 20 cents, weaker than consensus of 28 cents.

Aegion (AEGN -1.12%) reported Q3 adjusted EPS of 32 cents, below consensus of 35 cents.

FreightCar America (RAIL +0.54%) tumbled 10% in after-hours trading after it reported Q3 EPS of break-even, well below consensus of 12 cents.

Gasoline futures (RBZ16 +11.07%) surged over 10% in overnight Globex trading after Colonial Pipeline’s right of way, the biggest U.S. gasoline pipeline in the U.S., was shut down after an explosion and fire in Shelby County, Alabama.

Instructure (INST +1.64%) plunged 2% in after-hours trading after it reported Q3 adjusted revenue of $30.1 million, below consensus of $30.3 million, and said it sees Q4 revenue of $30.4 million-$31.0 million, below consensus of $32.2 million.

Monday’s Key Earnings

Anadarko Petroleum (NYSE:APC) -2.4% AH after missing estimates.

Dominion Resources (NYSE:D) +2.3% on earnings beat, Questar acquisition.

Southern Co. (NYSE:SO) +1.7% following positive guidance.

Williams Cos. (NYSE:WMB) -1.6% despite strong results.

Today’s Economic Calendar

FOMC meeting begins

Auto Sales

8:55 Redbook Chain Store Sales

9:45 PMI Manufacturing Index

10:00 ISM Manufacturing Index

10:00 Construction Spending

2:00 PM Gallup US ECI

Today’s Earnings here

Other…

today’s upgrades/downgrades from briefing.com

this week’s Earnings

this week’s Economic Numbers

One thought on “Before the Open (Nov 1)”

Leave a Reply

You must be logged in to post a comment.

well aussie, looks as if the martians are having the upper hand..