Good morning. Happy Monday. Hope you had a good weekend.

The Asian/Pacific markets closed mixed. China, Singapore, Australia and New Zealand did well; Indonesia and Malaysia were weak. Europe is currently mostly down. Italy is down 1.7%; France, Austria, Belgium, the Netherlands, Norway, Sweden and Greece are also weak. Futures in the States point towards a mixed and flat open for the cash market.

—————

LB Weekly – the indexes, the breadth indicators, a look at the big picture

—————

The dollar is up. Oil and copper are down. Gold and silver are up. Bonds are up.

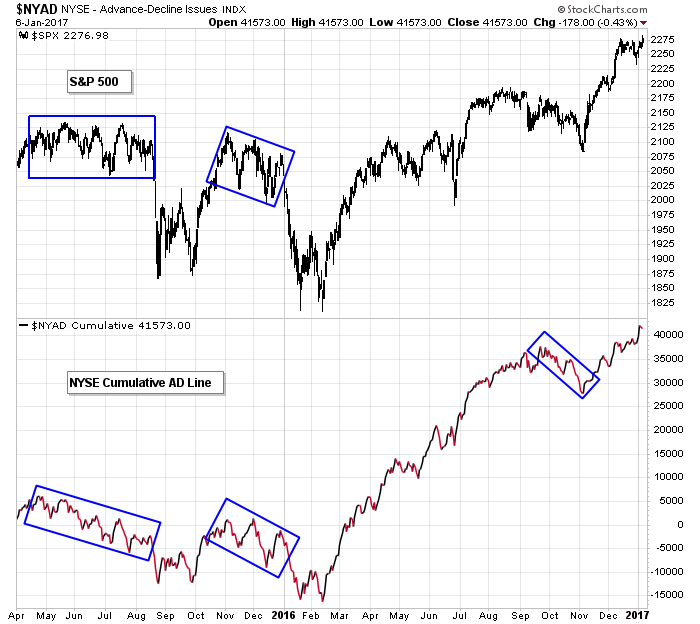

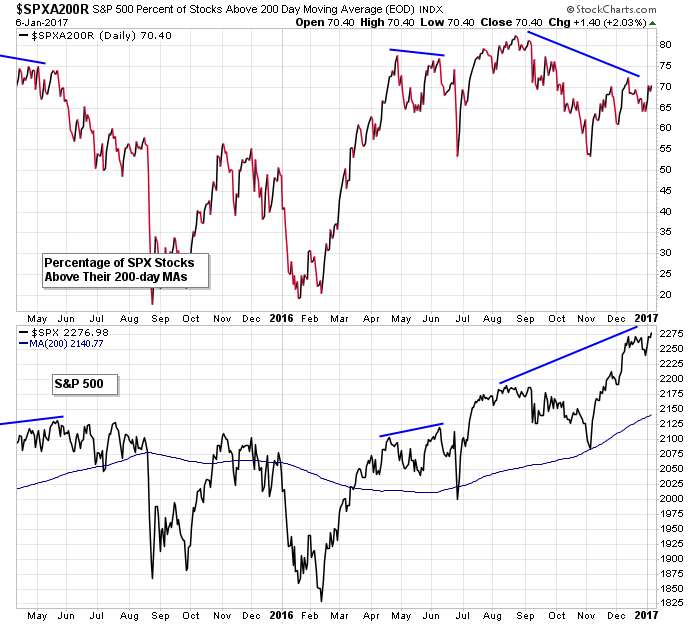

Last week several indexes moved to all-time highs. Some indicators fully support the price action; others are doing well but lagging a little.

For example, the cumulative AD line, which typically trends down for a few weeks before a minor correction plays out, or trends down for a few months before a major pullback takes place, hit a new high last week. This indicator fully supports the price action and does not hint at trouble brewing.

On the other hand, despite the market being at new highs, the percentage of SPX stocks above their 200-day moving averages is lower today that it was during most of the spring and summer. It’s not in bad shape; it’s just not as high as you’d expect given how well the market has done and the fact that the S&P is 6.4% above its own 200-day.

Overall I like the market. Anything goes in the near term, but for now dips remain buyable. More after the open.

Stock headlines from barchart.com…

Coca-Cola (KO -0.02%) was downgraded to ‘Sell’ from ‘Neutral’ at Goldman Sachs.

VMware (VMW +2.57%) was downgraded to ‘Neutral’ from ‘Buy’ at UBS.

Dr Pepper Snapple (DPS -0.48%) was upgraded to ‘Neutral’ from ‘Sell’ at Goldman Sachs with a 12-month target price of $93.

Hormel (HRL +0.50%) was initiated with an ‘Overweight’ at Piper Jaffray with a 12-month target price of $40.

Teva Pharmaceutical Industries Ltd. (TEVA -7.53%) was downgraded to ‘Market Perform’ from ‘Outperform’ at Wells Fargo.

Eagle Pharmaceuticals (EGRX -8.55%) was downgraded to ‘Underperform’ from ‘Neutral’ at Mizuho Securities USA with a 12-month target price of $64.

Ameriprise Financial (AMP +1.69%) was upgraded to ‘Outperform’ from ‘Neutral’ at Credit Suisse with a price target of $152.

Oasis Petroleum (OAS -1.95%) was upgraded to ‘Outperform’ from ‘Neutral’ at Macquarie Research with a 12-month target price of $19.

Endologix (ELGX -7.92%) said a patient death does not appear to be related to its AFX device and that the patient that died experienced a “Type 1B endoleak” which is usually due to natural disease progression. ELGX had fallen over 7% Friday after a FDA report showed the patient’s death may have been due to its AFX system.

Fiat Chrysler Automobiles (FCAU +6.22%) slid 1% in after-hours trading after it recalled over 86,000 older-model SUVs to replace driver and passenger-side airbags.

Aquinox Pharmaceuticals (AQXP +3.68%) lost over 1% in after-hours trading after it registered 10.5 million shares for holders.

Quidel (QDEL -0.63%) dropped over 6% in after-hours trading after it reported preliminary Q4 revenue of $52 million-$53 million, below consensus of $64.1 million.

Stage Stores (SSI -2.68%) tumbled 10% in after-hours trading after it said comparable store sales fell -7.3% for the 9-week period ending December 31 and then said it sees a 2017 adjusted loss of -70 cents to -85 cents a share, a wider loss than a November 17 estimate of -15 cents to -40 cents.

Today’s Economic Calendar

10:00 Labor market condition index

12:30 PM TD Ameritrade IMX

12:40 PM Fed’s Lockhart speech

3:00 PM Consumer Credit

Other…

today’s upgrades/downgrades from briefing.com

this week’s Earnings from Morningstar

this week’s Economic Numbers/Reports powered by ECONODAY

One thought on “Before the Open (Jan 9)”

Leave a Reply

You must be logged in to post a comment.

Watch China’s debt level. Oh yes, no carriers at sea? Watch events carefully now thru the swearing in.

Down futures this AM.