Good morning. Happy Tuesday.

The Asian/Pacific markets closed mostly down. India dropped 2.4%, and Singapore, Australia and South Korea fell more than 1%. China rallied 1.7%. Europe is currently mixed. Italy, Spain and Russia are up more than 1%; Germany, Amsterdam, Stockholm and Prague are down about 0.5%; Greece is down 0.9%. Futures here in the States point towards a down open for the cash market.

FREE ebook -> Powerful Stock Setups (I wrote one of the chapters)

The dollar is down. Oil and copper are up. Gold and silver are up. Bonds are down.

The market was all over the place yesterday but still contained within the high and low boundaries established a week ago when the market sold off hard on Tuesday and then rallied back on Wednesday. In fact the S&P has traded within the range the last three days and has made no progress in either direction.

The small caps haven’t improved [relative to the large caps], and the breadth indicators are worse off. So if anything, while the market has traded range bound, beneath the surface, things have deteriorated some.

My bias remains to the downside. Until these items improve (the small caps and the internals), rallies should be sold.

I saw an interesting note on Seeking Alpha. M&A activity in May hit an all-time high. The previous two high water marks? May 2007 and January 2000 – both just a couple months before major tops were put in place.

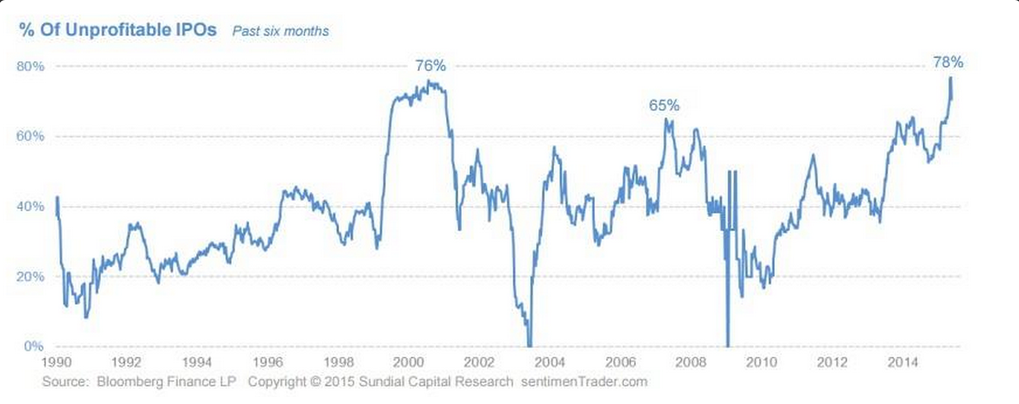

I saw this chart posted recently. The percentage of unprofitable IPOs has exceeded the 2000 and 2007 highs – the two previous highs.

Be careful out there.

Stock headlines from barchart.com…

Intel (INTC -1.63%) was downgraded to ‘Market Perform’ from ‘Outperform’ at BMO Capital.

Big Lots (BIG +2.26%) was upgraded to ‘Overweight’ from ‘Equal Weight’ at Barclays.

Iron Mountain (IRM +0.99%) was downgraded to ‘Underperform’ from ‘Hold’ at Jefferies.

Medtronic PLC (MDT +0.50%) reported Q4 EPS of $1.16, higher than consensus of $1.12.

Dollar General (DG +0.30%) reported Q1 EPS of 84 cents, better than consensus of 81 cents.

Glenview Capital reported a 7.06% stake in Manitowoc (MTW +2.33%) .

Whiting Petroleum (WLL -1.55%) was initiated with a Buy at Evercore ISI with a price target of $45.

Prudential (PRU -0.34%) was initiated with an ‘Overweight’ at Piper Jaffray with a price target of $106.

AIG (AIG +0.12%) was initiated with an ‘Overweight’ at Piper Jaffray with a price target of $73.

Anadarko (APC +0.28%) was initiated with a ‘Buy’ at Evercore ISI with a price target of $100.

Palo Alto (PANW +0.60%) was initiated with a ‘Buy’ at Guggenheim with a price target of $200.

Point72 Asset reported a 5.1% passive stake in Renewable Energy (REGI +16.46%) .

PVH Corp. (PVH +0.04%) reported Q1 adjusted EPS of $1.50, better than consensus of $1.38, and then raised guidance on fiscal 2015 adjusted EPS view to $6.85-$6.95 from $6.75-$6.90, above consensus of $6.86.

Earnings and Economic Numbers from seekingalpha.com…

Today’s economic calendar:

Auto sales

8:30 Gallup US ECI

8:55 Redbook Chain Store Sales

10:00 Factory Orders

Notable earnings before today’s open: CBRL, CONN, DAKT, DG, MDT, SOL

Notable earnings after today’s close: ABM, AMBA, ASNA, GES, GIII, GWRE, NCS, VMEM

Other…

today’s upgrades/downgrades from briefing.com

this week’s Earnings

this week’s Economic Numbers

{kind=link}

0 thoughts on “Before the Open (Jun 2)”

Leave a Reply

You must be logged in to post a comment.

Yesterdays comeback had me scratching my head. I was only a few points away from where I predicted a bounce but nothing as large as we experienced.

I do agree with Jason that we are on the edge of down draft.